The COP Delusion: Decades of empty words and no action

February 7, 2024

‘Business as usual’ overrides action to protect humanity’s future

In an opinion article published in Climate & Capitalism on January 26, Alan Thornett accused critics of the United Nations’ COP28 meetings in Dubai of “leftist posturing.” The left must, he wrote, “recognize the positive role that the UN has played in global warming over the last 35 years.”

In an opinion article published in Climate & Capitalism on January 26, Alan Thornett accused critics of the United Nations’ COP28 meetings in Dubai of “leftist posturing.” The left must, he wrote, “recognize the positive role that the UN has played in global warming over the last 35 years.”

“Only governmental action — and action taken by governments prepared to go on a war footing — can make the changes necessary to stop climate change in the limited time we have left, and only the UN COP process has a chance of achieving it.”

The following article was not written as a reply to Thornett, but it could well have been. It was posted as a thread on X (formerly Twitter) on February 7, by Stephen Barlow (@SteB777), who describes himself as a “naturalist, conservationist, environmentalist and nature photographer.” I was not familiar with his views before this, but his critique of the COP-focused approach to stopping climate change is powerful, and to me convincing.

Climate & Capitalism welcomes further debate and discussion on this subject.

—Ian Angus

COP: MEANINGLESS WORDS AND NO ACTION

To even think about the climate and ecological crisis, let alone address it, we need to completely rethink our whole approach, and wipe the slate clean.

This is because for the last 50 or so years we assumed our governments would respond rationally.

We have had the 1972 UN Environment conference, and its action plan. We had the Brundtland Commission Report, Our Common Future (1987) and the 1992 Rio Earth Summit, largely based on this.

On each occasion our leadership appeared to largely agree with the summary, and agreed to take action. But then none of that promised action, ever took place. Yes, we see a lot of hollow words at the COP talks, but it’s all been meaningless.

It’s been meaningless, because our governments never did anything to actually change direction, and the identified adverse trends, just got worse and worse. They only said they’d act, to make it look like they were acting.

I can sum up the problem very simply. At the 1992 Rio Earth Summit, the UNFCCC was signed, which set up the COP talks. The aim was to phase out the burning of fossil fuels. But we’ve burned more fossil fuels since 1992, than prior to 1992.

Self-evidently, this was not the expected outcome. I can tell you with 100% certainty, that the situation now, was never envisaged in 1992. I know this, because I warned this would likely happen, and no one took any notice of me. All said I was wrong.

The basic underlying problem, was that [we assumed] governments and politicians respond rationally to evidence of a serious danger and address it. I mean, we’ve all seen the disaster movies, about how governments prepare and come together to address crisis.

Except, the difficulty, is that there is no historical precedent for governments actually acting like this, to protect humanity. It’s a cultural myth, a fallacy, about what governments actually are, and how they react.

Governments aren’t there to protect the public, as they falsely claim. Governments are just there to facilitate the business as usual (BaU) model developed after the industrial revolution. To protect the interests of the powerful benefiting from this. Nothing more.

The only time governments appear to act in the interests of their people, is if there’s a potential invasion of their country, or a major immediate crisis like a pandemic, financial crash. Yet the main motivation is to protect BaU, not to protect the people.

A country’s people are essential for maintaining BaU, and governments only seem to be trying to protect the people, because that’s necessary to maintain BaU, not because people matter.

If you don’t believe me, just look at the ongoing UK COVID Inquiry, where you see the whole focus was on protecting the economy, and the then PM was quite willing to sacrifice the lives of older people, to that aim.

The allies, only eventually cooperated in WW2, because Nazi Germany, and Japan, were an existential threat to their economies and countries, not to protect the public. But they needed the public on board, so it looked like they were protecting the public.

The climate and ecological crisis is more than enough proof of what they say, and governments have never even nearly cooperated to address the crisis. They just do the bare minimum, to give the impression of it, because their people are concerned about it.

Therefore, the first assumption which needs to be scratched, is the mistaken assumption that if you give governments enough scientific evidence, that they’ll act appropriately. Self-evidently they don’t.

Scientists have largely wasted their time for the last 30 years, giving sincere advice and evidence to governments, not the slightest bit interested in phasing out fossil fuels, or stopping biodiversity loss.

I must make it very clear, that I’m not saying the scientific work of the scientists was wasted, just the giving it to governments, and mistakenly thinking they’d act appropriately.

A massive amount of energy has been wasted on trying to convince politicians, who didn’t want to be convinced. The present economic model, is wholly predicated on the burning of fossil fuels, and the unsustainable use of natural resources.

They’re not going to be persuaded to stop what they’re doing, by inconvenient evidence. Of course they’re going to say they’re going to act, because opinion polls show the majority are worried about climate change.

The first rules of effective problem solving is acknowledging the problem exists, then understanding the problems, and potential obstacles to solving, so you don’t waste energy on ineffective solutions.

Essentially governments are there, to facilitate an economic model predicated on fossil fuel extraction and burning, and the unlimited extraction of natural resources. They’re not interested in stopping it, and instead, protecting the public. That’s not what governments are.

I’m not saying just give up. I’m saying realizing it’s a fools errand trying to persuade governments to do the right thing. We’ve got 30-50 years of empirical evidence to tell us this is a thorough waste of time.

Therefore, we need to do 2 things.

Firstly, persuade the public, that governments are not acting in their interests.

Secondly, instead of just trying to persuade governments to do the right thing, we have to force them to do the right thing.

The approach above can only work, once people accept what the problem/situation is. The difficulty is that most are stuck in the mindset of still trying to persuade politicians and governments to act, when they have no intention of acting.

People will not try to force their governments into action, whilst they still mistakenly believe their government is acting in their interest, and we just need to be a bit more persuasive, and argue the case better.

If people simply accepted, or a large consensus did, that governments and politicians are not acting in their interests. This alone would be a massive impetus for governments and politicians, to change how they act. They know, they rely on the people.

But as long as people believe that governments, politicians, Elon Musk and Bill Gates etc, are acting in their best interests, these rulers, won’t be motivated to change direction. They think people are gullible because they believe their lies.

The rulers would be mighty worried, if they thought people saw through them. In fact, this attempt to usher in authoritarian fascism, seems to be them being driven by this fear. As long as people are falling for the authoritarian schtick, they’d try playing this game.

It’s difficult to persuade everyone to see things like that. However, it is about time scientists and other influential people, started telling the public, spelling it out to them, that our leadership is putting us in grave danger.

@KevinClimate [Kevin Anderson] has often spoken about how so called climate professionals, don’t want to rock the boat, presumably advance their careers. Certainly, @ClimateHuman is well aware of this problem.

Although this is about persuading the public of the serious danger we are in, it’s no good just activists telling the public this, because scientists need to speak out, journalists also, and all those with influential platforms.

It’s all about the dynamics of influence. It’s very easy for governments, politicians and the oligarch media, to “other” activists, and say don’t take any notice of them, they’re just eco-loons. But if scientists, and other people the public trust, spoke out en masse. …

You see, at the moment, the public is misled. They think the situation can’t be that serious, or all those scientists and other influential people in the know, would be shouting it from the rooftops. But they’re not.

This appears to confirm the false message that only the “eco-loon” activists see it as a big danger, because the scientists who know, aren’t sounding the alarm. Giving the impression, the danger is exaggerated. This appears to confirm the false message that only the “eco-loon” activists see it as a big danger, because the scientists who know, aren’t sounding the alarm. Giving the impression, the danger is exaggerated.

There’s much else that needs to be re-evaluated, in our regrouping. But I’ve already gone on too long in this thread. So I will save it for another day.

https://climateandcapitalism.com/2024/0 ... no-action/

700 million years ago, the Earth froze. Now we know why.

February 9, 2024

All-time low CO2 levels produced the longest and coldest ice age in in Earth’s history

Between 717 and 660 million years ago, the Earth was covered in snow and ice—a 57 million year ice age. Geoscientists have found the likely cause: all-time low levels of volcanic carbon dioxide in the atmosphere. (Image: NASA)

For reference: the next time someone claims there isn’t enough CO2 in the air to affect our planet’s climate….

Australian geologists have determined what most likely caused an extreme ice-age climate in Earth’s history, more than 700 million years ago. The study, published in Geology, helps our understanding of the functioning of the Earth’s built-in thermostat that prevents the Earth from getting stuck in overheating mode. It also shows how sensitive global climate is to atmospheric carbon concentration.

“Imagine the Earth almost completely frozen over,” says the study’s lead author, ARC Dr. Adriana Dutkiewicz.

“That’s just what happened about 700 million years ago; the planet was blanketed in ice from poles to equator and temperatures plunged. However, just what caused this has been an open question. We now think we have cracked the mystery: historically low volcanic carbon dioxide emissions, aided by weathering of a large pile of volcanic rocks in what is now Canada; a process that absorbs atmospheric carbon dioxide.”

The project was inspired by the glacial debris left by the ancient glaciation from this period that can be spectacularly observed in the Flinders Ranges in South Australia. A recent geological field trip to the Ranges, led by co-author Professor Alan Collins from the University of Adelaide, prompted the team to use computer models to investigate the cause and the exceptionally long duration of this ice age.

The extended ice age, called the Sturtian glaciation after the 19th-century European colonial explorer of central Australia, Charles Sturt, stretched from 717 to 660 million years ago, a period well before the dinosaurs and complex plant life on land existed.

Various causes have been proposed for the trigger and the end of this extreme ice age, but the most mysterious aspect is why it lasted for 57 million years—a time span hard for us humans to imagine.

The team went back to a plate tectonic model that shows the evolution of continents and ocean basins at a time after the breakup of the ancient supercontinent Rodinia. They connected it to a computer model that calculates CO2 degassing of underwater volcanoes along mid-ocean ridges—the sites where plates diverge and new ocean crust is born.

They realized that the start of the Sturtian ice age precisely correlates with an all-time low in volcanic CO2 emissions. In addition, the CO2 outflux remained relatively low for the entire duration of the ice age.

At that time, there were no multicellular animals or land plants on Earth. The greenhouse gas concentration of the atmosphere was almost entirely dictated by CO2 out-gassing from volcanoes and by silicate rock weathering processes, which consume CO2.

Co-author Dietmar Müller from the University of Sydney:

“Geology ruled climate at this time. We think the Sturtian ice age kicked in due to a double whammy: a plate tectonic reorganization brought volcanic degassing to a minimum, while simultaneously a continental volcanic province in Canada started eroding away, consuming atmospheric CO2. The result was that atmospheric CO2 fell to a level where glaciation kicks in—which we estimate to be below 200 parts per million, less than half today’s level.”

The team’s work raises intriguing questions about Earth’s long-term future. A recent theory proposed that over the next 250 million years, Earth would evolve towards Pangea Ultima, a supercontinent so hot that mammals might become extinct.

However, the Earth is also currently on a trajectory of lower volcanic CO2 emissions, as continental collisions increase and the plates slow down. So, perhaps Pangea Ultima will turn into a snowball again.

Dr. Dutkiewicz comments: “Whatever the future holds, it is important to note that geological climate change, of the type studied here, happens extremely slowly. According to NASA, human-induced climate change is happening at a pace 10 times faster than we have seen before.”

Includes materials provided by the University of Sydney.

https://climateandcapitalism.com/2024/0 ... -know-why/

*****

EU Farmers’ Protests, Food Security, and the Green New Deal Big Lie by Omission About Livelihoods

Posted on February 8, 2024 by Yves Smith

Perhaps yours truly is unduly skittish, or perhaps simply not sufficiently familiar with EU farm policies. But as we’ll discuss soon, a recent Financial Times editorial on farmers’ protests in Europe made me wonder if something is missing from my, and perhaps others’, perspective on the pressures intensifying on how societies provision themselves on a collective and individual level. Put it another way, the article bugged me and I’ve been puzzling out why.

Specifically, as the Financial Times’ headline whinges in the editorial, The rise of agricultural populism, a critically important group of suppliers is balking at the prospect of green/carbon-output-reducing reforms hurting their incomes. The pink paper concedes that even with large EU subsidies, farmers work hard for typically not very good pay levels, and that has already been under stress.

Now as an editorial, one would expect this piece to be aimed particularly at Serious People, as in the decision-making or at least influencing sort. But a striking result is the assumption of the “We are all adults here, these problems can be sorted out” tone underplays how the farmers v. climate policy fight may be a canary in the coal mine of intractable climate change issues. These current and upcoming choices are already difficult but are made even more so by living in a market/neoliberal society.

The Green New Deal and others who are seeking climate change action have done themselves and the planet a huge disservice via their rainbows and unicorns approach to policies. They have pointedly avoided the notion that sacrifices need to be made. The subtext is that if consumers merely make smarter choices, like buying EVs, using bicycles more often, installing heat pumps, insulating, and support investments like wind turbines and high speed trains, the worst will be forestalled. Admittedly, some do advocate more hair-shirt-y measures, like giving up on or reducing the consumption of beef, air travel, and indoor temperature control. Notice the huge hidden assumption: that consumers are well off enough to be able to make choices, as opposed to get by, and on top of that, they can afford higher costs, and/or to front big-ticket expenses that promise to offer a good return.

What the Green types have (as far as I can tell) chosen to ignore is the impact on livelihoods of aggressive climate change action. For instance, there’s a great deal of hand-wringing about Bitcoin energy consumption. Yet there’s a dearth of proposals to outlaw Bitcoin and severely criminalize its use. That seems to be due to bizarre deference to Mr. Market, as if speculation is more important than preserving the environment, along with perhaps a reluctance to throw people in the crypto sphere out of work. Similarly, no one is willing to very aggressively tax (say via super duper high landing fees) private jets so as to greatly reduce their use. Until the rich are willing to give up on their greenhouse gas spewing perk perks, it’s not hard to see why dull normals can be persuaded that climate change is a con.

The Green types are even less honest in discussing the impact of climate-saving policies on many workers. The talk up new green jobs. But most people do not want to be thrown out of work (or face such worsened employment conditions that their current employment becomes close to untenable) and then scramble to remake themselves. Even if they come out economically whole in the end, they face a great deal of stress and income pressure in between. And if they are carrying debt, that could mean bankruptcy, selling their house, or other major upheaval. Let us not forget that stress is bad

for your health and your relationships. The costs extend beyond the purely financial.

Those around long enough remember the promised benefits of NAFTA. Americans were told it would create new jobs. In fact, NAFTA shrank employment. The other flavor of happy talk around globalization is that everyone winds up net ahead, so policies can be devised to take from the winners and share with the losers. But I have yet to see any Robin Hoods in senior positions in government. The fallback to that is to blame those who wound up on the bad end of policy changes as deplorables, unwilling to move where jobs are (as if they can magically land them in cities where they have no contacts and have to front travel and lodging costs) To the extent there has been a policy response, it’s been “let them eat training” and only lately, poorly thought out protectionism.

Add to that, as social scientists have ascertained, the political center of gravity tends to move to the right in bad economic times. People are more concerned than ever with hanging on to what they have, which dovetails with conservative messaging. Some also wind up falling back on traditional structures like family and religious organizations. And since the 2008 crisis, those at the top have pulled away even as social safety nets have frayed and class mobility has collapsed. Intensified class and income disparity are not great foundations for advocating for or imposing costs on those lower in the food chain and expecting them to submit quietly.

Now it is not wrong to depict many in the so-called right of exploiting discontent of the downtrodden lower orders. But it should be obvious that they would not be able to do so if the supposed left were credibly attempting to watch their backs. And as we can see with climate change, the left has shown itself to be indifferent to the sacrifices it expects ordinary workers to make, and has done a terrible job of demanding even more from the carbon-hogging rich, much the less engaging in much more than virtue signaling displays themselves.

The spectacle of farmers’ protests against climate changes and environmental diversity polices spreading across Europe is reminiscent of the Gillet Jaunes protests….except the farmers collectively are crucial suppliers and at least for now also seem able to engage in collective action.

And despite the “Cooler heads will prevail” tone of the piece, recent headlines suggest EU officials are in considerable retreat. This seems particularly peculiar since members of the pink paper’s comment section maintain that farmers were consulted before various measures were proposed. The protests and the policy changes suggest otherwise….or alternatively, if they were “consulted,” they weren’t much listened to. These are from the Financial Times:

Brussels bows to farmers’ protests by slashing environmental targets February 6

EU backs down on agricultural emissions after farmers’ protests February 5

EU leaders pledge more concessions to appease angry farmers February 1

Brussels struggles to placate farmers as far right stokes protests January 25

We have the conundrum in the EU, which I don’t pretend to understand, of substantial farm subsidies, on the order of €60 billon a year, yet the Financial Times agrees that most farmers find it hard to get by:

Some other sectors suggest farmers have always been coddled by the EU. Yet in all but the largest enterprises, farming at the best of times involves big risks and meagre rewards. Farmers say that in recent years input and borrowing costs have soared thanks to inflation and the war in Ukraine. Margins have been squeezed by retailers trying to hold down prices in the cost of living crisis. And they complain of being undercut by imports, including Ukrainian products as the EU has — rightly — thrown open its doors to support Kyiv’s economy.

Some of this may be due to the EU having higher standards for food production than the US. Some of the subsidies are to support exports. But many farmers are in the uncomfortable position of being laborers on their own plantations.

Despite acknowledging that many farmers are under enough duress that they are in no mood to take more, the pink paper exhibits elite disconnect:

As with other parts of the green transition, Brussels and EU states need to find ways to hold firm to the overall goals while offsetting the impact on the most vulnerable groups — by phasing in measures over time, exempting smaller farms, or offering targeted support.

Given the importance of food security, moreover, a broader debate is needed on where in the supply chain the costs of going green should fall: on farmers, on taxpayers through even higher subsidies, or on consumers and the food and retail industry.

At least the Financial Times does not resort to the insulting US “having a conversation”. But this is what it amounts to. In the end, the fact that the farmers have already forced a considerable walkback shows that at least for now, like bankers, they know they have sufficient control of socially critical resources to not be pushed around, and even demand concessions.

One way that might…might..force a bit more realism is conjoint analysis, where individuals are offered paired choices to reveal what their real preferences are. Here, having experts and then the media serve up in concrete terms the implicit choices being made might instill a smidge more realism and importantly, fear. Instead of bloodlessly talking about what a X degree increase in 15 years looks like, show a series of expected results, particularly local ones, if that happens, versus what the results are if the increase is only some smaller level. Then if most agree they would rather not have X, but some less destructive Y (still making clear that lesser evil is still evil), show them further what options they have to get there. If we are going to play the “markets and choices” game, the time is long past when 50,000 foot happy talk is adequate.

And while on the topic of the need for more realisim, consider the next part of the Financial Times story:

With the number of EU farms falling due to consolidation as younger generations sell up, more private capital probably needs to be attracted into farming — as is happening, for example, in the US — which can invest in technology and reap economies of scale.

Some governments will fret about rural areas emptying out, increasing the burden on housing and services in cities. Yet, given the difficulty of making a living from farming today, turning farms into more stable businesses owned by companies that can afford to invest might just help to keep more people on the land.

Huh? First, “more technology” likely includes “more fertilizer” when the US is finding that intensive use of nitrogen fertilizers results in toxic nitrates, which are producing cancer cluster in the Corn Belt. And even though Russia has been blamed for tight fertilizer supplies (in fact, the cause is sanctions and the refusal of the West to exempt the Russian agricultural bank from sanctions so lower-income countries can make purchases), ammonia production is highly energy intensive and ammonia plants in Europe and the UK have been closing as a result. From an written answer to a question posed to the EU Commission in 2022:

Half of European ammonia production plant closed

Spiralling gas prices have caused a decline in European ammonia production, thereby aggravating the shortage of fertilisers in Europe. CRU Group analysts estimate that around half of European ammonia production plant and 33% of nitrogen fertiliser plant has closed down as a result

The Norwegian producer Yara International ASA has reduced its ammonia production to around a third and other plants in Europe have also reduced or suspended their fertiliser production. According to analysts, it has now become much cheaper to import ammonia into Europe than to produce it. If gas prices remain high, further pushing up the cost of fertilisers, farmers will probably start to purchase less, limiting yields and cultivated areas.

Yours truly does not know how much, if any, capacity has been restored now that energy prices have moderated. But longer-term, higher energy prices, whether natively or as a result of higher taxes and fees, are necessary to deter use. Greener energy is not free; it has different resource costs, such as environmental degradation and toxic leftovers, than CO2-generating sources. Collectively, we need to go on an energy diet and no one wants to hear that.

But the more obvious sour note in the Financial Times extract above is that capital, which will almost certainly expect higher returns than owner-operators, aka farmers, do now, and can magically reduce labor content so as to also provide for better to pay to serfs, um, farm labor. Members of the Financial Times comments section were quick to call that out:

LK

Yet, given the difficulty of making a living from farming today, turning farms into more stable businesses owned by companies that can afford to invest might just help to keep more people on the land.

Only someone who has never worked or even visited a farm would say this.

And would investment from a business rearrange the seasons to consistent units of work that can be evenly distributed across the year and be paused for holidays?

Stop pipes from bursting overnight?

Make calving and lambing occur only during weekday, working hours?

No salaryman will do the work required of a farmer.

A.J. Maher

Well we all know the enormous contribution Agri business has made to the building of European civilisation…Oh no, .. wait.

It is also a display of touching naivety to think that, once family farming has been taken over by corporate farming, the demands for subsidy will disappear. Business will leach off the taxpayer far more efficiently than the “patrons” ever could. In that respect at least, business is already far outperforming the traditional family farm sector as it sucks up the Lions share of subsidies.

There comes a point when Liberal economics becomes a pathology. This editorial is an exhibition of that pathology….

Humans have a tendency to go on tilt when faced only with unattractive alternatives. But the pretense that not acting is not tantamount to a choice increase the odds that outcomes will not just be bad, but the worst.

https://www.nakedcapitalism.com/2024/02 ... anism.html

******

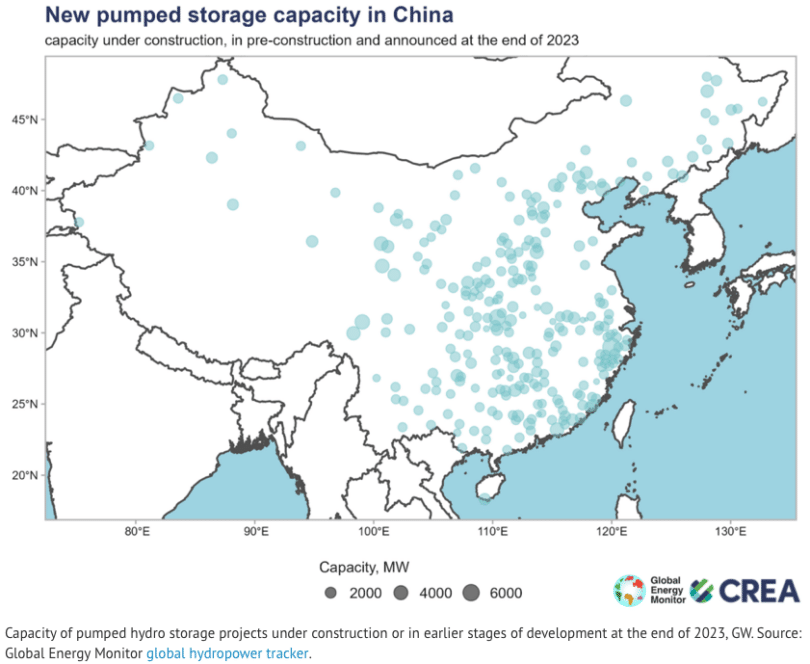

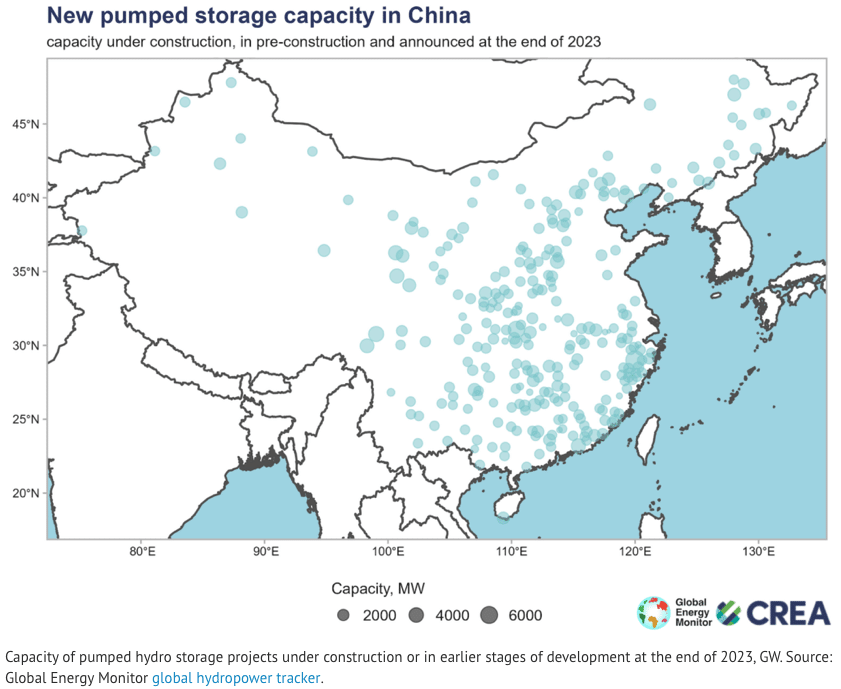

Capacity of pumped hydro storage projects under construction or in earlier stages of development at the end of 2023, GW. (Photo: Global Energy Monitor global hydropower tracker)

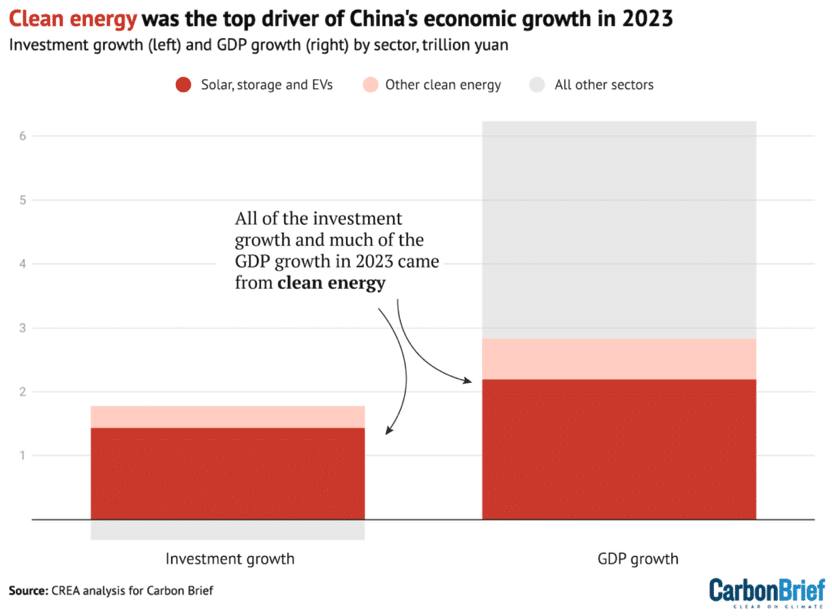

Analysis: Clean energy was top driver of China’s economic growth in 2023

Originally published: Carbon Brief on January 25, 2024 by Lauri Myllyvirta (more by Carbon Brief) | (Posted Feb 09, 2024)

The new sector-by-sector analysis for Carbon Brief, based on official figures, industry data and analyst reports, illustrates the huge surge in investment in Chinese clean energy last year—in particular, the so-called “new three” industries of solar power, electric vehicles (EVs) and batteries.

Solar power, along with manufacturing capacity for solar panels, EVs and batteries, were the main focus of China’s clean-energy investments in 2023, the analysis shows.

(For this analysis, we used a broad definition of “clean energy” sectors, including renewables, nuclear power, electricity grids, energy storage, EVs and railways. These are technologies and infrastructure needed to decarbonise China’s production and use of energy.)

Other key findings of the analysis include:

Clean-energy investment rose 40% year-on-year to 6.3tn yuan ($890bn), with the growth accounting for all of the investment growth across the Chinese economy in 2023.

China’s $890bn investment in clean-energy sectors is almost as large as total global investments in fossil fuel supply in 2023—and similar to the GDP of Switzerland or Turkey.

Including the value of production, clean-energy sectors contributed 11.4tn yuan ($1.6tn) to the Chinese economy in 2023, up 30% year-on-year.

Clean-energy sectors, as a result, were the largest driver of China’ economic growth overall, accounting for 40% of the expansion of GDP in 2023.

Without the growth from clean-energy sectors, China’s GDP would have missed the government’s growth target of “around 5%”, rising by only 3.0% instead of 5.2%.

The surge in clean-energy investment comes as China’s real-estate sector shrank for the second year in a row. This shift positions the clean-energy industry as a key part not only of China’s energy and climate efforts, but also of its broader economic and industrial policy.

However, the spectre of overcapacity means China’s clean-energy investment growth—and its investment-driven economic model, in general—cannot continue indefinitely.

The growing importance of these new industries gives China a significant economic stake in the global transition to clean-energy technologies.

Yet it also poses questions for overseas policymakers attempting to tie their own climate strategies to domestic industrial growth.

Clean energy drives China’s growth in 2023

The ‘new three’ dominate clean-energy investment

Solar power

Wind power

Electric vehicles

Energy efficiency

Electricity storage and hydrogen

Railways

Nuclear power

Electricity grids

Why clean energy took off in 2023

What clean-energy growth means for China—and the world

Clean energy drives China’s growth in 2023

China’s clean-energy investment boom means the sector accounted for all of the growth in investment across the country’s economy in 2023, with spending in other areas shrinking.

China invested an estimated 6.3tn yuan ($890bn) in clean-energy sectors in 2023, up from 4.6tn yuan in 2022, a 1.7tn yuan (40%) year-on-year increase. In total, clean energy made up 13% of the huge volume of investment in fixed assets in China in 2023, up from 9% a year earlier.

With Chinese investment growing by just 1.5tn yuan in 2023 overall, the analysis shows that clean energy accounted for all of the growth, while investment in sectors such as real estate shrank.

This is shown in the figure below, which also highlights the concentration of clean-energy investment in the so-called “new three” of solar, energy storage and EVs.

Clean energy was also the top contributor to China’s economic growth overall, contributing around 40% of the year-on-year increase in GDP across all sectors.

Contributions to the growth in Chinese investment (left) and GDP overall (right) in 2023 by sector, trillion yuan. “New three” refers to solar, EVs and storage. (Photo: Centre for Research on Energy and Clean Air (CREA) analysis for Carbon Brief. Chart by Carbon Brief)

Including the value of goods and services, the clean-energy sector contributed an estimated 11.4tn yuan ($1.6tn) to China’s economy in 2023, an increase of 30% year-on-year.

This means clean energy accounted for 9.0% of China’s GDP in 2023, up from 7.2% in 2022.

Without the contribution of clean-energy sectors to China’s economic growth in 2023, the country would have seen its GDP rise by just 3.0%, instead of the 5.2% actually recorded.

This would have missed government growth targets at a time of increasing concerns over the nation’s economic prospects, amid the ongoing real-estate crisis and declining population.

The major role that clean energy played in boosting growth in 2023 means the industry is now a key part of China’s wider economic and industrial development.

This is likely to bolster China’s climate and energy policies—as well as its “dual carbon” targets for 2030 and 2060–by enhancing the economic and political relevance of the sector.

The ‘new three’ dominate clean-energy investment

This analysis is based on a combination of government releases, industry data and analyst reports, with the exact methodology varying sector-by-sector, as set out in the sections that follow.

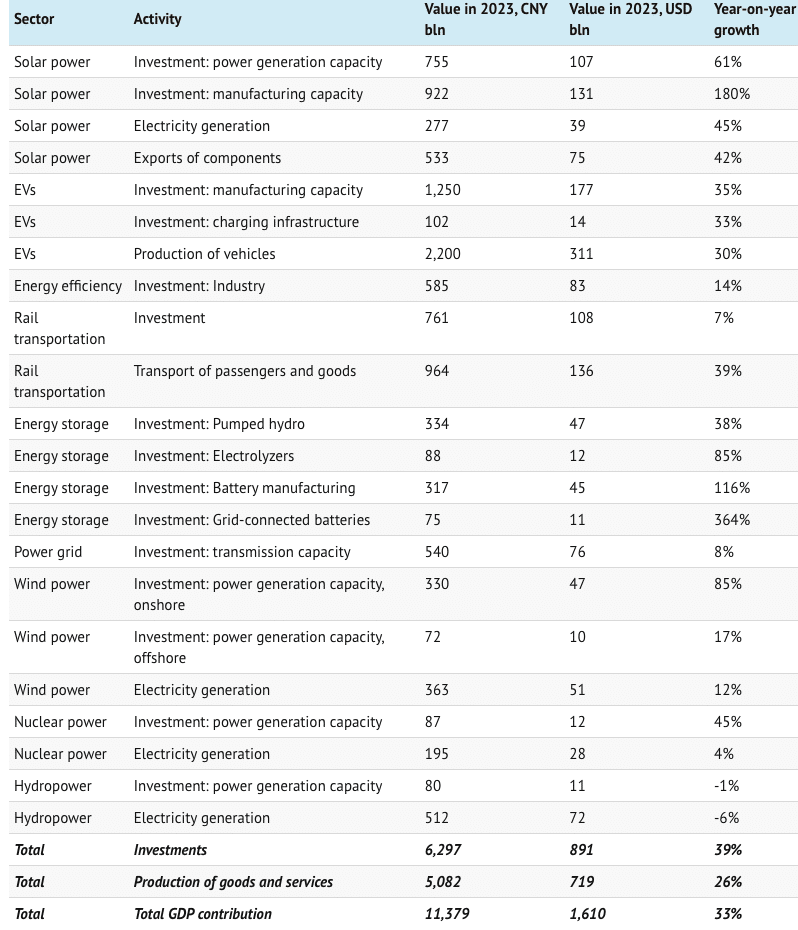

The table below lists the estimated contributions of each sector to Chinese investment and GDP overall in 2023, as well as the year-on-year growth since 2022.

The analysis includes solar, EVs, energy efficiency, rail, energy storage, electricity grids, wind, nuclear and hydropower within the broad category of “clean-energy sectors”. All of these are technologies and infrastructure needed to decarbonise China’s energy supply and consumption.

The so-called “new three” of solar, storage and EVs are all prominent in the table—and all recorded strong growth.

Our analysis shows that investment in clean power generation and energy storage capacity reached 1.7tn yuan in 2023 (up 48% year-on-year), while investment in manufacturing capacity for solar, EVs and batteries reached 2.5tn yuan (+60%).

Investment in clean-energy infrastructure reached 1.4tn yuan (+9%, comprising grids, EV charging points and railways) and investment in energy efficiency was 600bn yuan (+15%).

Meanwhile, our analysis shows the value of production of goods and services in the clean-technology sectors reached 5.1tn yuan in 2023, increasing 26% year-on-year.

This includes the value of electricity generation, EV sales and solar exports, as well as the transport of passengers and goods via rail.

Solar power

Solar was the largest contributor to growth in China’s clean-technology economy in 2023. It recorded growth worth a combined 1tn yuan of new investment, goods and services, as its value grew from 1.5tn yuan in 2022 to 2.5tn yuan in 2023, an increase of 63% year-on-year.

While China has dominated the manufacturing and installations of solar panels for years, the growth of the industry in 2023 was unprecedented.

On the installation side, two major central government initiatives drove increased volumes, namely the “whole-county distributed solar” and the “clean energy base” programmes.

In addition, in response to the slowdown in the real-estate sector, the central government introduced a new policy at the start of 2023, to encourage the development of solar power industries on unused and existing construction lands.

Meanwhile, during the annual legislative meetings in the spring of 2023, 15 provinces prioritized solar industry development in their government work agendas.

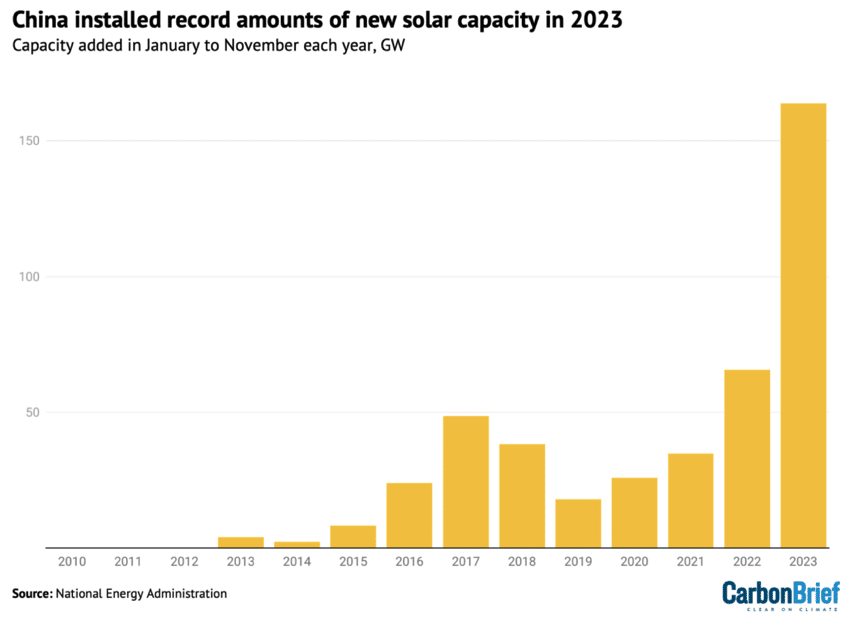

Detailed data on the growth in China’s solar installations in the first 11 months of the year is shown in the figure below. (An estimated 200GW was added across the country during 2023 as a whole, more than doubling from the record of 87GW set in 2022.)

Solar capacity newly installed in China in January to November each year, gigawatts. (Photo: National Energy Administration. Chart by Carbon Brief)

At the same time, China’s solar manufacturing industry recorded even stronger growth in 2023. China added 340 gigawatts (GW) of polysilicon production capacity and 300GW of wafer, cell and module production capacity in 2023, according to the International Energy Agency (IEA).

China experienced a significant increase in solar product exports in 2023. It exported 56GW of solar wafers, 32GW of cells and 178GW of modules in the first 10 months of the year, up 90%, 72% and 34% year-on-year respectively, according to the China Photovoltaic Industry Association. However, due to falling costs, the export value of these solar products only increased by 3%.

Within the overall export growth there were notable increases in China’s solar exports to countries along the “belt and road”, to southeast Asian nations and to several African countries.

For this analysis, the value of investments in new solar manufacturing capacity was estimated from the average capital costs of each step in the supply chain, taken from a compilation of reported project costs. This gave a significantly lower cost level than reported in other literature.

The analysis assumes that local government investment in facilities and infrastructure, as well as direct subsidies, added 30% to the reported private investment.

Investment in solar power was estimated by multiplying the newly added capacity from Bloomberg New Energy Finance by the unit investment costs for rooftop and utility-scale systems from China Photovoltaic Industry Association.

The value of exported solar power equipment was based on China Photovoltaic Industry Association data for 2022 and reported export growth for 2023.

The value of solar power equipment produced for domestic installation was not included in our analysis, to avoid overlap with the already-estimated investment costs for domestic solar projects.

Wind power

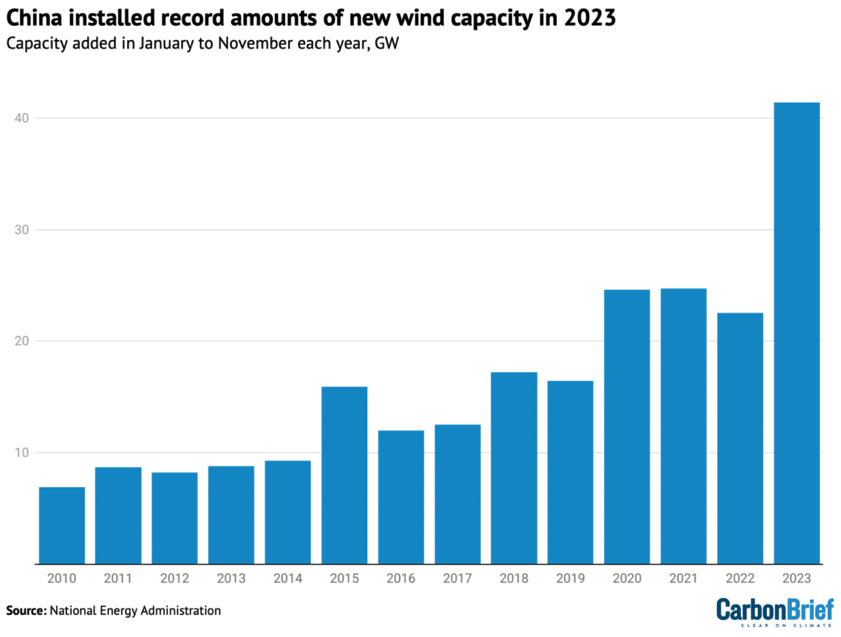

China installed 41GW of wind power capacity in the first 11 months of 2023, an increase of 84% year-on-year in new additions. Some 60GW of onshore wind alone was due to be added across 2023, according to China Galaxy Securities, based on trends in previous years.

In addition, offshore wind capacity increased by 6GW across the whole of 2023.

Wind capacity added in the first 11 months of each year is shown in the figure below.

Wind capacity newly installed in China in January to November each year, gigawatts. (Photo: National Energy Administration. Chart by Carbon Brief)

By the end of 2023, the first batch of “clean-energy bases” were expected to have been connected to the grid, contributing to the growth of onshore wind power, particularly in regions such as Inner Mongolia and other northwestern provinces. The second and third batches of clean-energy bases are set to continue driving the growth in onshore wind installations.

The market is also being driven by the “repowering” of older windfarms, supported by central government policies promoting the model of replacing smaller, older turbines with larger ones.

The potential for distributed wind power is also being explored, with initiatives such as the “villages wind utilisation action” being planned for active implementation.

Progress on offshore wind power construction in 2023 got off to a slow start. This is a reflection of a shift from nearshore to deeper offshore projects and from single projects to larger bases.

Offshore wind projects are also facing complex approval processes, involving multiple regulatory aspects, leading to uncertainties and slower-than-expected installations.

However, these issues are being addressed and the fourth quarter of 2023 saw a rebound in offshore wind construction, with 2024 expected to be a significant year for project deliveries.

Since 2021, new wind projects in China no longer receive subsidies from the central government.

Despite technological advancements reducing costs, increases in raw material prices have resulted in lower profit margins compared to the solar industry, leading to a smaller overall investment in wind power relative to solar power.

Electric vehicles

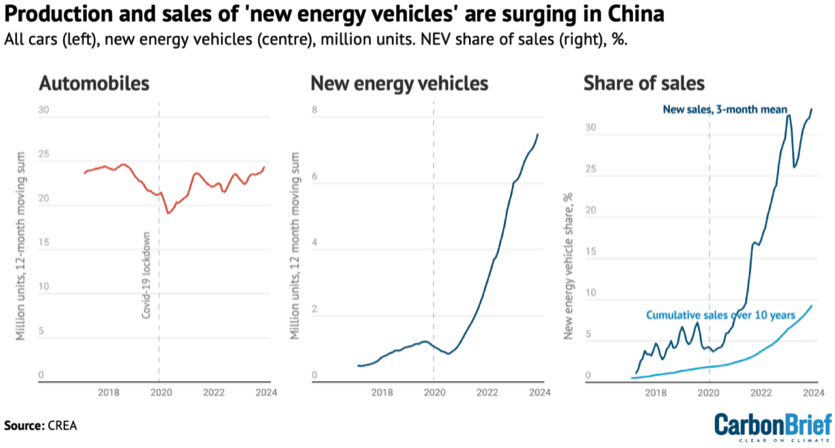

China’s production of electric vehicles grew 36% year-on-year in 2023 to reach 9.6m units, a notable 32% of all vehicles produced in the country.

The vast majority of EVs produced in China are sold domestically, with sales growing strongly despite the phase-out of purchase subsidies announced in 2020 and completed at the end of 2022.

The national purchase subsidy for EVs was a central government finance instrument that had been fostering the EV market for 13 years. Its demise highlights a gradual shift from policy-driven to market-driven demand, making growth more likely to be sustained.

Sales of EVs made in China reached 9.5m units in 2023, a 38% year-on-year increase. Of this total, 8.3m were sold domestically, accounting for one-third of Chinese vehicle sales overall, while 1.2m EVs were exported, a 78% year-on-year increase.

The growth of “new energy vehicle” (NEV, mainly EVs) production and sales is shown in the figure below, which also shows their rising share of all vehicles sold.

Production and sales of all vehicles and “new energy vehicles” (NEVs) in China, from National Bureau of Statistics and China Association of Automobile Manufacturers data via Wind Financial Terminal. NEVs include battery electric vehicles and plug-in hybrids. The right-hand side shows the share of NEVs out of all new vehicles sold, and the cumulative share over the preceding 10 years, as an indicator of the share of NEVs out of vehicles on the road. (Chart by Carbon Brief)

China’s EV market is highly competitive, with at least 94 brands offering more than 300 models. Domestic brands account for 81% of the EV market, with BYD, Wuling, Chery, Changan and GAC among the top players.

Sustaining this growth has required major investment in manufacturing capacity.

This analysis estimates investments in EV manufacturing capacity based on a study by China International Association for Promotion of Science and Technology (CIAPST), which put investment in EV manufacturing at 0.7tn yuan in 2021.

The analysis assumes that EVs accounted for all of the growth in investment in vehicle manufacturing capacity reported by China’s national bureau of statistics (NBS) in 2022 and 2023, while investment in conventional vehicles was stable

This implies that investment in EV manufacturing reached CNY 1.2tn yuan in 2023. This is likely to be conservative, because production volumes for combustion engine vehicles are falling, implying a corresponding fall in investment.

This analysis accounts for the expansion of battery manufacturing capacity separately—alongside electricity storage—even though it is being driven by the growth in EV production.

The analysis estimates the value of EV production, including both domestic sales and exports, based on vehicle production volumes from NBS and the reported average EV price.

These EV prices include the value of batteries produced for EVs, so the value of battery production is not included separately.

Meanwhile, EV charging infrastructure is expanding rapidly, enabling the growth of the EV market. In 2022, more than 80% of the downtown areas of “first-tier” cities—megacities such as Beijing, Shanghai and Guangzhou—had installed charging stations, while 65% of the highway service zones nationwide provided charging points.

More than 3m new charging points were put into service during 2023, including 0.93m public and 2.45m private chargers. The accumulated total by November 2023 reached 8.6m charging points.

This analysis puts investment in EV charging infrastructure at 0.1tn yuan in 2023, based on an estimated average cost of 30,000 yuan per charging point.

Energy efficiency

China’s energy intensity reduction targets have put pressure on industries to reduce their energy use per unit of output, spurring investment in more efficient processes.

For this analysis, the size of the market for energy service companies is used as a proxy for investment in energy efficiency in industries and buildings. This market grew to an estimated 0.6tn yuan in 2023, up from 0.5tn yuan in 2022, based on the revenue growth of the top 10 listed energy service companies ranked by market capitalization, for the first two or three quarters of 2023.

Over the past two decades, China’s energy service sector has experienced rapid expansion, growing from 1.8bn yuan in 2003 to 607bn yuan in 2021. Investment in the industrial service sector has been a key driver, accounting for about 60% of the total investment.

However, 2022 saw a significant downturn in the industrial energy service output, influenced by poor industrial growth, even though the building service sector continued expanding.

This analysis puts China’s investment in building energy efficiency at 80bn yuan per year. The country’s 14th five-year plan for energy savings in buildings and development of “green buildings” targets 80m square metres per year of renovated and newly built green buildings.

Compared with the almost 1,000m square metres of building space completed annually, this is a small percentage, and accordingly, the estimated value of total investments is modest.

Electricity storage and hydrogen

China is rapidly scaling up electricity storage capacity. This has the potential to significantly reduce China’s reliance on coal- and gas-fired power plants to meet peaks in electricity demand and to facilitate the integration of larger amounts of variable wind and solar power into the grid.

The construction of pumped hydro storage capacity increased dramatically in the last year, with capacity under construction reaching 167GW, up from 120GW a year earlier.

This growth is illustrated in the figure below, which shows pumped hydro capacity under construction or in earlier stages of development at the end of 2023.

Data from Global Energy Monitor identifies another 250GW in pre-construction stages, indicating that there is potential for the current surge in capacity to continue.

For this analysis, estimated annual investments in pumped storage are assumed to be proportional to the capacity under construction, while the reported construction cost of 6 yuan per watt is spread over three years. This implies that investment in 2023 amounted to 0.3tn yuan.

Construction of new battery manufacturing capacity was another major driver of investments, estimated at 0.3tn. This is based on the added capacity reported by the China Automotive Power Battery Industry Innovation Alliance and estimated average investment costs per unit of production capacity, taken from a compilation of publicly reported project costs.

Investment in electrolysers for “green” hydrogen production almost doubled year-on-year in 2023, reaching approximately 90bn yuan, based on estimates for the first half of the year from SWS Research. Analyst reports and compilations of projects published in news media put far larger numbers on China’s investments in green hydrogen, but these generally include the spending on electricity generation, which in this analysis is accounted for separately.

Investment in “new energy storage technologies”—a classification dominated by batteries—more than doubled in 2023, reaching 75bn yuan. This estimate is based on newly added capacity in 2023 reported by China Energy Storage Alliance and average investment costs calculated from National Energy Administration data.

Railways

China’s ministry of transportation reported that investment in railway construction increased 7% in January—November 2023, implying investment of 0.8tn for the full year. This includes major investments in both passenger and freight transport. Investment in roads fell slightly, while investment in railways overall grew by 22%.

The share of freight volumes transported by rail in China has increased from 7.8% in 2017 to 9.2% in 2021, thanks to the rapid development of the railway network.

In 2022, some 155,000km of rail lines were in operation, of which 42,000km were high-speed. This is up from 146,000km of which 38,000km were high-speed in 2020.

The value of passenger and freight transportation on China’s railways increased by 39% year-on-year in 2023, reaching nearly 1tn yuan.

Nuclear power

In 2023, 10 nuclear power units were approved in China, exceeding the anticipated rate of 6-8 units per year set by the China Nuclear Energy Association in 2020 for the second year in a row.

There are 77 nuclear power units that are currently operating or under construction in China, the second-largest total in the world. The total yearly investment in 2023 was estimated for this analysis at 87bn yuan, an increase of 45% year-on-year, based on data for January—November from the National Energy Administration.

The highest numbers of nuclear projects are located in coastal provinces with large concentrations of heavy industry, such as Guangdong, Fujian and Zhejiang, as the development of inland nuclear power projects remains stalled.

These provinces get around 20% of their electricity from nuclear power and continue to expand the technology as part of their efforts to cut emissions from their power sectors.

Electricity grids

China’s power-sector development plans include a major increase in inter-provincial electricity transmission capacity and numerous long-distance transmission lines from west to east.

State Grid, the government-owned operator that runs the majority of the country’s electricity transmission network, has a target to raise inter-provincial power transmission capacity to 300GW by 2025 and 370GW by 2030, from 230GW in 2021. These plans play a major role in enabling the development of clean energy bases in western China.

China Electricity Council reported investments in electricity transmission at 0.5tn yuan in 2023, up 8% on year—just ahead of the level targeted by State Grid.

Why clean energy took off in 2023

The clean-energy investment boom in 2023 is the outcome of a major pivot in China’s macroeconomic strategy. As this analysis shows, investment flowed from real estate into manufacturing—primarily in the clean-energy sector.

Total investment in the manufacturing industry increased by 9% year-on-year in 2023, while investment in the power and heat sectors climbed 23%. These increases were entirely due to growth in investment in clean energy, with investment in other areas falling. Therefore, China’s pivot into manufacturing was, in reality, a pivot to cleantech manufacturing.

The reason for this pivot was the contraction in the real-estate sector, where investment fell by 10% year-on-year in 2022 and another 9% in 2023. While this drop was in line with the government’s aim to address financial risks and excess leverage in the sector, it left a major hole in aggregate investment demand and in the revenue of China’s local governments.

Local governments were under pressure to attract investment, meaning that they offered generous subsidies and helped arrange financing.

The central government, for its part, eased private-sector access to financial markets and bank loans during the Covid-19 pandemic, facilitating the growth of the clean-energy sector.

Unlike the state-owned firms dominating traditional industries, the low-carbon sector, largely composed of private companies, gained access to previously constrained credit.

The significance of this economic shift is reflected not only in the figures revealed by this analysis but also in the language being used by Chinese media.

The three largest of clean-energy sectors by value, namely solar, storage and EVs, are being referred to as the “new three”, in contrast to the “old three”—clothing, home appliances and furniture.

This pivot was only possible because China’s clean-energy policies and wider industrial policy had built the foundation and scaled up these sectors so that they were primed for rapid growth.

The post-Covid credit “push” for clean energy growth also coincided with a demand “pull”, driven by falling costs and the increased competitiveness of low-carbon technologies against fossil fuels due to technological advancements.

Moreover, the announcement in 2020 of the 2060 carbon neutrality target had raised expectations and provided the political signal for the scale-up.

What clean-energy growth means for China—and the world

Clean technology has been an important part of China’s energy policy, industrial strategy and climate change efforts for a long time. Last year marked the first time that the sector also became a key economic driver for the country. This has important implications.

China’s reliance on the clean-technology sectors to drive growth and achieve key economic targets boosts their economic and political importance. It could also support an accelerated energy transition.

The massive investment in clean technology manufacturing capacity and exports last year means that China has a major stake in the success of clean energy in the rest of the world and in building up export markets.

For example, China’s lead climate negotiator Su Wei recently highlighted that the goal of tripling renewable energy capacity globally, agreed in the COP28 UN climate summit in December, is a major benefit to China’s new energy industry. This will likely also mean that China’s efforts to finance and develop clean energy projects overseas will intensify.

Globally, China’s unprecedented clean-energy manufacturing boom has pushed down prices, with the cost of solar panels falling 42% year-on-year—a dramatic drop even compared to the historical average of around 17% per year, while battery prices fell by an even steeper 50%.

This, in turn, has encouraged much faster take-up of clean-energy technologies.

Projections of solar power deployment, in particular, have been upended. The IEA’s latest World Energy Outlook introduced an additional global energy scenario just to look at the implications, projecting that if global deployment of solar power and grid-connected batteries follows the expansion of manufacturing capacity, then global power-sector coal use and carbon dioxide emissions could be a sizable 15% lower than in the base case by 2030. Most of the additional deployment of solar in the IEA’s revised projections is in China.

Even with the increased deployment, however, there is a limit to how much solar power, batteries and other clean technology can be absorbed, as the manufacturing expansion has already saturated most of the global market.

This means that the expansion will run into overcapacity, if maintained. On the other hand, in order to keep driving growth in investment, clean-technology manufacturing would need to not only absorb as much capital as it did in 2023, but keep increasing investment year after year.

The clean-technology investment boom has provided a new lease of life to China’s investment-led economic model. There are new clean-energy technologies where there is scope for expansion, such as electrolysers.

Eventually, however, entirely new sectors will have to be found for investment–or China’s economic model will have to be transformed once there is nowhere left for investment to flow.

The manufacturing boom also cements China’s dominant position in clean-energy supply chains. Other countries therefore face a choice of whether they want to benefit from the low-cost supply of solar panels, batteries, EVs and other clean-energy technology from China.

The alternative is diversifying their supply and paying the cost of building new supply chains, in the form of subsidies and import tariffs required to enable domestic producers or producers in third countries to compete against Chinese suppliers. Such efforts would further increase supply and push down global prices even further.

https://mronline.org/2024/02/09/analysi ... h-in-2023/